Foreword

As a council leader I am all too aware of the undeniable economic impact the COVID-19 pandemic has had on our high streets and town centres. With restrictions explicitly closing non-essential retail, hospitality venues, personal care businesses, entertainment and cultural venues – all those places that line our streets and town centres, combined with longer trends such as increasing online sales, it’s unsurprising that in November 2020 the local data company predicted that there could be 15,000 additional net vacancies (empty shops) in Britain.

Vacancies are not just caused by the pandemic and are unlikely to ever be a ‘single issue problem’. They can be caused by a number of challenges. Overall, average retail unit vacancy rates in the UK have been increasing since 2018, due in part to the rise of online shopping, as well as more localised difficulties. For a number of years, many councils across England’s regions have been dealing with increasing vacancy rates, as well as the high social and financial costs associated with this.

There are however many good examples of where councils have used ‘hard’ and ‘soft’ approaches to deal with empty shops in town centres and high streets. These examples can be replicated across a number of different contexts. Case studies included in this good practice guide range from fast and responsive actions such as Bath & North East Somerset Council introducing local art commissions into the windows of local vacant units, to substantial, long-term investments like Sheffield City Council and their work to re-use a former department store and transform it into a tech hub. Optimistically, as councils take a key role in steering their high streets and town centres towards more mixed use futures that are less retail-dependent, there are also opportunities for innovation and delivery of public good that may not previously have been possible on such scale. It is also worth remembering that in most places, large parts of town centres will be privately owned and finding solutions will involve working with the private sector and encouraging investment from them.

High streets are notoriously difficult contexts in which to effect change, with multiple stakeholders and interests that cross local authority jurisdictions and departmental divides. By learning from others who have taken a wide range of approaches to addressing the multi-faceted issue of retail vacancy, the intention is that this guide will provide a resource that can support action at all scales, from market towns to major metropolitan centres. We hope you find this a useful document.

Cllr David Renard, Chair of the LGA’s Economy, Environment, Housing and Transport Board

Introduction

The COVID-19 pandemic and associated lockdowns have resulted in a significant impact on high streets and town centres across the UK, although the challenge of vacancy has been apparent for a number of years. Combined with long-term trends affecting retail, such as increases in online sales and a growing focus on the ‘experience economy’, the impact is that many high street businesses are reducing their presence in town centres or closing altogether, leaving vacant property in their wake with negative long-term consequences for these places.

The LGA commissioned We Made That to produce this good practice guidance that can be used by councils to help enact change and tackle vacancy on high streets and in town centres. The guidance highlights and contextualises past and current vacancy trends, details hard and soft powers available to councils, and presents the following action framework of different methods councils have used to tackle vacancy. Specific and detailed good practice case studies from areas across the UK are presented within this framework to further illustrate each method.

- Business/grant funding.

- Direct council delivery.

- Restoration.

- Meanwhile use/pop up.

- Business support.

- Policy intervention.

- Change of use.

- Redevelopment.

A list of further reading and guidance can be found at the bottom of the page.

About this guide

This guidance presents good practice case studies within a framework for tackling vacancy. It presents an approach to vacancy as an existing challenge, rather than preventative measures. This guidance was written in early 2021, and whilst contemporary data regarding the impacts of the COVID-19 pandemic has been used, the full extent of its influence remains to be seen.

Context

Increasing vacancy and COVID-19

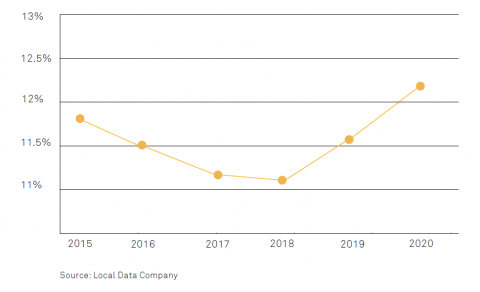

Overall, average retail unit vacancy rates in the UK have increased since 2018, despite having decreased between 2015-2018. The table below shows the average UK shop vacancy from 2015 - 2020, combining high streets, shopping centres and business parks.

Overall GB vacancy rate (all location types) 2015 - 2020

According to data from the Office for National Statistics, retailing currently accounts for an average of around 33 per cent of addresses on high streets, the second highest use after residential, which accounts for an average of around 55 per cent. In most regions and countries, around 10 per cent of addresses are offices and around 2 to 3 per cent are leisure or community facilities. The figures across Britain remain similar to 2019, although there is a slight rise in the proportion of residential addresses, around 1 to 2 per cent across most regions and countries. The proportion of retail addresses has fallen across Britain by similar amounts.

There are both social and financial costs associated with empty shops. For example, vacant shops cost London’s economy an estimated £350 million according to data from the Greater London Authority (through loss of business rates, loss of earnings and the subsequent cost of unemployment and job seekers allowance). Further to this, empty shops can cause a ‘negative feedback loop’ which means they discourage investment, decrease the offer of a high street, prevent consumers from visiting and contribute to a general sense of decline and neglect.

Local Data Company data shows that nearly 12 per cent of retail sites were unoccupied in first half of 2019, with chains hit by rising costs and low consumer confidence. This was the highest percentage recorded since 2015. Major chains shrank dramatically in this period, with 3,508 fewer sites operating compared with a fall of 2,848 in the first half of 2018. Independent stores proved more resilient; only a net 138 closed in the first six months of 2019 as entrepreneurial businesses including mobile phone stores, nail salons, bars and cafés took advantage of cheaper retail rents to expand. Health and beauty services cannot be delivered online and therefore survived the rise of internet shopping, though the impacts of lockdown restrictions on these sectors have been severe and the long-term impacts remain to be seen.

Data from retail analyst Springboard suggests that more UK high street stores are now shuttered than at any time in the past six years. The vacancy rate on high streets was 12.2 per cent in quarter one of 2020 (LDC). The vacancy rate was 14.1 per cent for Shopping Centres (14.4 per cent in Dec 2019); and 8.2 per cent for retail parks (8.1 per cent in Dec 2019).

A net 7,834 outlets closed or vacated the property in the first half of 2020, which is an increase of 115 per cent from the first half of 2019. This decline could be attributed directly to shoppers choosing to buy online during the pandemic and resulting UK lockdowns, and low consumer confidence. Springboard data has shown that the number of shoppers on UK high streets in August 2020 was 38.3 per cent lower than in August 2019. In May 2020, a third of all retail sales were online (previously one fifth), according to the Office for National Statistics.

The Local Data Company figures show that 11,120 chain operator outlets had closed by October 2020, with 5,119 shops opening, creating a net decline of 6,001, almost double the decline tracked last year (3509). Independent high street businesses situated on local high streets close to residential pockets have proved more resilient than chain stores during the high street lockdown. Fewer than 1 per cent disappeared in the first half of the year as those working from home now do their shopping and socialising close to where they live, by comparison with chain stores which tend to attract shoppers from further afield.

Beyond 2020

The evidence shows that changes are likely to lead to the rise of multifunctional town centres, with empty shops being given over to other productive uses, in an acceleration of existing trends.

Following the announcement of the second national UK lockdown, beginning on the 5 November 2020, Local Data Company analysts warned that vast numbers of leisure and hospitality businesses may have to close for good. This would leave 14 per cent of high street, retail park and shopping centre outlets vacant in Britain which would be the highest level since the LDC began its survey. At the time of this report, just over 13 per cent of those premises were vacant. LDC reported a best case scenario of 15,000 more outlets left vacant in 2020, compared with 9,169 net closures in 2019.

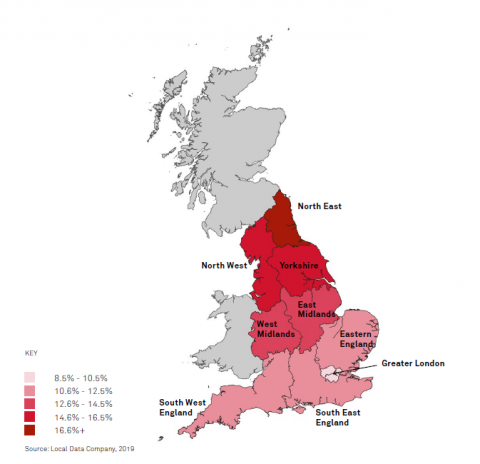

The data for the map below, taken from the Local Data Company, shows the average vacancy rate for high street shops in 2019 by percentage. Greater London has the lowest vacancy rate at 8.9 per cent whilst the North East has the highest vacancy rate at 16.7 per cent. There is a clear pattern of higher vacancy levels the further north the area, although recent findings from the Local Data Company show a small cluster of high levels of vacancy around Blackpool (19.1 per cent) and Wigan (20.8 per cent). The same data also shows a small cluster of high vacancy in Eastern England just outside of Greater London in Basildon (18.8 per cent) and Southend (18.4 per cent).

Regional variation

The map above shows the average vacancy rate for high street shops in 2019 by percentage across the UK. Greater London has the lowest vacancy rate at 8.9 per cent whilst the North East has the highest vacancy rate at 16.7 per cent. There is a clear pattern of higher vacancy levels the further north the area, although recent findings from the Local Data Company show a small cluster of high levels of vacancy around Blackpool (19.1 per cent) and Wigan (20.8 per cent). The same data also shows a small cluster of high vacancy in Eastern England just outside of Greater London in Basildon (18.8 per cent) and Southend (18.4 per cent).

Planning policy context

This guidance comes in the context of changing national planning policy. These key changes are highlighted below, along with intended benefits and possible challenges.

New Permitted Development Rights (PDRs) in effect from 31 August 2020

The Government introduced new PDRs in August 2020, which is the right to carry out certain building works and changes of use without having to make a planning application. The new PDRs enable the following changes of land use and building works without the need for planning permission:

- Build up to two floors of upward extensions on top of existing post-war homes, terraces, offices, and shops.

- Demolish light industrial or office buildings that have been vacant for six months or more and do not exceed 1000 square meters in footprint, and replace them with residential development.

The new PDRs do not apply if the building is in a conservation area, an area of outstanding natural beauty, a site of special scientific interest, a national park, the broads or a world heritage site. It remains that listed buildings cannot be demolished without planning permission.

Prior approval of some issues is still required from the council, including:

- traffic and transport impacts

- whether your new building will overlook or have an effect on the privacy of its neighbours

- the appearance of the new building

- the effect on local heritage

- landscaping

- whether the noise from nearby commercial premises will affect residents

- whether adding housing to the area will affect local businesses.

The new PDRs have the intended benefit of building more homes to meet high demand whilst reducing long-term vacancy, but there are many concerns that this will lead to unacceptable standards of development. In terms of high street health, whilst residential uses for vacant properties on high streets and in town centres could bring some benefits for the local population and drive additional footfall, there are challenges and risks associated with this, such as inactive frontages and a lack of flexibility for future change of use.

Changes to the Use Class Order in England from 1 September 2020

The 2020 changes to the Use Class Order introduced new use classes E, F1, and F2, which group together several different uses previously contained in separate classes. Of particular relevance is the new Class E that has replaced previous classifications commonly found on high streets and in town centres. Class E includes A1 Shops, A2 Financial and professional services, A3 Restaurants and cafés, B1(a) Office, B1(b) Research and development of products or processes, B1(c) Light industrial processes, parts of D1 Non-residential institutions and parts of D2 Assembly and leisure. By grouping the heterogeneous town centre uses within a single use class, the legislation hopes to support adaptability and, in turn, the viability of high streets by removing the need to apply for planning permissions.

Although this change aims to allow for more flexibility, as no planning applications will be needed in many cases, this will reduce the councils’ ability to manage change in their high streets. Councils in most cases would prefer to be able to assess the benefits and detriments of a proposed Change of Use through a planning application process, particularly in order to take into account wider strategic priorities such as high street regeneration or public health objectives. At the time of publication the Government is also consulting on a new permitted development right to allow any retail or office space to be converted to residential use in high streets and town centres with no protection for conservation areas.

White Paper ‘Planning for the Future’

For some time, the Government has been signaling its intention to make radical changes to the planning system in England. The COVID-19 pandemic brought about some immediate changes to certain aspects of planning policy – such as enabling pubs to offer hot food takeaway services – while other, substantial changes to the planning process, aimed at creating a new system suitable for the 21st century, are the subject of the White Paper ‘Planning for the Future’ which details the government’s proposals.

The intention of the proposals are reforms of the planning system to streamline and modernise the planning process, bring a new focus to design and sustainability, improve the system of developer contributions to infrastructure, and ensure more land is available for development. If approved however, the planning system will move from discretionary to a rule-based system. This could diminish the role of local planning authorities’ and communities’ ability to shape their areas based on agreed priorities in their local plan.

What powers do councils have to tackle vacancy?

Hard powers

Hard powers that can contribute to tackling vacancy refer to the wide range of statutory powers of councils, they can be summarised as follows:

Planning tools

Local planning authorities (LPAs) have the ability to write strategic policies for their places and determine planning applications against those policies. Whilst not relevant to all levels of authority, borough councils, county councils and unitary authorities are generally responsible for these tasks. For long-term change to tackle vacancy, a clear policy position is essential. This may be set out at the following levels of policy hierarchy:

Local plans - Succinct and up-to-date local plans should provide a positive vision for the future of each area and a framework for addressing housing needs and other economic, social and environmental priorities such as high street and town centre regeneration, which may include strategic positions on appropriate provision, scale and type of retail in response to evidence around vacancy.

Supplementary planning documents - These are documents which add further detail to the policies in the local plan. They can be used to provide further guidance for development on specific sites, such as individual town centres, or on particular issues, such as shop front design.

Local Development Order - Local Development Orders (LDOs) simplify the planning process in certain areas by allowing the council to grant automatic planning permission for some kinds of development. Effectively they extend Permitted Development Rights (PDRs) within a defined area.

Town centre frameworks or strategies - Town centre frameworks aim to create the right environment for vibrant town centres. They can identify opportunities to enhance the public realm, improve accessibility and support the provision of shops and services at a finer-grain and more specific level than other policy ‘tiers’. Most town centre frameworks are subject to community engagement in order to identify the requirements of each individual centre. Such documents provide the basis for managing and promoting positive change in identified town centres. They may be formally adopted by the council or may remain as unadopted guidance. Whatever their status, the presence of a robust, holistic and locally-specific strategy for a town centre that has the support of local stakeholders is an essential tool allowing high streets and town centres to meet their full potential. Vacancy may be one of many issues that are addressed through such a process.

Development management powers - Once the ‘rules’ have been set in policy, local planning authorities use their development management powers to ensure that policy is followed and that development is compliant with their stated aspirations. Councils therefore have powers to manage any project or development that requires planning consent. In the case of empty shops, Change of Use consent has historically been a key point of management, although this control has now been limited, as described above.

Asset management

It is common for councils to hold ownership of town centre and high street properties. These may be dedicated retail units, mixed-use blocks that also contain housing or part of a wider portfolio of libraries and other civic assets. According to the Cabinet Office, council fixed assets were worth £515 billion in the year 2019/2020. Effective asset management of both vacant and in-use buildings plays a major role in delivering better outcomes for citizens, and creating a sense of place. Powers related to asset management include:

Control of existing and retained assets - Whilst individual councils vary enormously in the size and nature of their asset holdings, they all face similar challenges, such as filling or letting vacant properties. By prioritising asset management, removing silos within the authority, working with a variety of partners, and assessing whether the asset base is performing at its optimum, councils will be more able to use their assets to meet these challenges.

Acquisition and control of ‘problem’ assets - There are a range of methods for filling vacant property that is council-owned, detailed in the case studies in the action framework below. If the council does not own the vacant property, it can be bought either through a straightforward transaction agreed with the owner (to take control of the freehold or a fixed-term lease), or in rare and extreme cases through the use of a Compulsory Purchase Order (CPO) which government policy stipulates should be used only as a last resort. CPOs give councils the legal right to obtain land or property without the consent of the owner, but are required to pay the owner compensation which usually includes the value of the property and any relocation costs. Before a CPO is confirmed, councils will have to show that they have taken steps to encourage the owner to bring the property into acceptable use. Councils can also make use of the Town and Country Planning Act 1990, section 226 which allows the authority to take control of land for community use. The powers in section 226 are intended to help councils which have planning powers to take control of the land they need to put in place their community strategies and local development documents. These planning powers are wide enough to allow the council to take over land for redevelopment.

Community asset transfer - The joint Local Government Association (LGA) and Locality guide on empowering communities by making the most of local assets, offers councils guidance on enabling the improved use of underused public buildings by transferring their ownership. Such community asset ownership harnesses the creativity and commitment of local residents and creates sustainable enterprises that provide local services and contribute to the economic and social wellbeing of town centres.

A key lesson is to engage with the council’s asset strategy and be clear about the business case and wider benefits for any proposed interventions. Revenue from commercial lettings can be a key source of income for councils, so there is pressure for council-owned high street property to generate revenue. Commercial property can either be commercially let with proceeds used for other council priorities or may be let for under more commercially favourable ‘social value leases’ with specified measurable social value outputs. In the case of problematic vacant units, such terms may make units more accessible to start-up and smaller scale enterprise who would not otherwise be in a position to access properties, which can have dual benefits of reducing vacancy and supporting local business.

Powers of investment

Councils have the power to invest in projects and schemes that tackle challenges such as empty shops, to support wider strategic priorities. Councils can also secure funding – for example from regional or national government. The action framework includes many good practice case studies in which councils have won funding, and have then used that money either directly for their own scheme, or distributed it to developers or trusts that are able to carry out redevelopment work or restoration work, in order to bring a vacant property back into use.

If money has been distributed in the form of grants distributed to third parties, councils can control the nature of the scheme through conditional grant agreements. Crucially this means that the council can, for example, stipulate the type of business or organisation that should take on an empty shop once it’s been brought back into use (see good practice case study from Sheffield City Council under ‘Redevelopment’).

Business rates relief – Whilst not ‘direct’ investment, consideration of rates relief schemes can encourage uptake of vacant property within town centres by reducing overheads for potential occupants.

Enforcement and licensing

High streets and town centres are places of a confluence of activity that can risk being ‘siloed’ between departments within councils. A place-based approach that brings together different departments to tackle challenges that can contribute to or exacerbate issues of vacancy is necessary. These issues can include property dilapidation, poor cleanliness and fly-tipping, and addressing them will typically involve a wider range of enforcement and licensing powers including:

- Empty Dwelling Management Orders

- Building Act 1984, Sections 77&78 – for emergency action to make dilapidated buildings safe, and ultimately occupiable.

- public health and waste management enforcement

- outdoor trading licenses to encourage street activity.

Democratic power

Councils have powers to shape how areas formally grow and develop. Councillors engage with residents and groups on a wide range of different issues and take on an important community leadership role, as well as contributing to the development of policies and strategies, including budget setting, and scrutinising council decisions or taking decisions on planning or licensing applications. It is through this role that councillors can identify the need to tackle vacancy and encourage or heavily influence the decision to formalise a policy and strategy for doing so, which then influences other hard powers, particularly within planning tools.

Soft powers

Soft powers refer to the influence, but not the statutory right, of a council to be able to effect development so that it aligns to their own strategic priorities for the benefit of the local population. They are powers that come with a civic leadership role that are influential in strategic thinking and policy making.

Facilitation

It is crucial that places have council strategies for future development. Involving stakeholders and organisations with similar goals that can help to coordinate these strategies promotes good relationships and good practice whilst also allowing councils to have a wider influence. Such council-facilitated groups can be informal, consisting of community groups, local businesses, the police and traders/business/sector associations, or may be formalised as business improvement districts (BIDs) or town teams.

Councils also have a role in convening town centre stakeholders, for example as holders of databases of vacant properties and their owners, or the contact details of businesses looking for units, that are used as tools to fill empty properties (see good practice case study example from Telford & Wrekin Council under ‘Business/Grant Funding’). In this case, the council holds no formal power but has a ‘match making’ role; by knowing of available vacant properties and which businesses are looking for units, the council can assign and fill the vacancies without needing to formally take on any leases themselves.

Place marketing and communications

Councils are able to use soft powers to promote place, for example to drive up footfall to high streets and create vibrancy and diversity that will attract new businesses to fill empty shops. The use of social media along with a strategy based on public engagement is a good method of promoting a high street at low cost (see good practice case study example from Bath and North Somerset Council under ‘Direct Delivery’).

The set up and use of virtual high streets where businesses trade via a consolidated website is growing, particularly in the context of COVID-19, as it helps drive a ‘shop local’ mentality as well as keeping businesses afloat until high streets are reopened safely (see good practice case study example from Telford & Wrekin Council under ‘Business/Grant Funding’).

Civic leadership

The civic leadership role of the council gives a degree of soft powers and the ability to influence decision making outside of formal council strategy. For example, What Walworth Wants is a catalogue of high street projects in Walworth, London funded by the London Borough of Southwark and the Greater London Authority. The document was developed as a public tool to be used by local residents, community groups, public authorities and other stakeholders to take ownership and co-deliver projects. The council is therefore part of the strategic process but does not have full formal management of the resulting delivery.

What support systems and funding sources are available to underpin action?

Support

The High Streets Task Force is an alliance of place making experts working to redefine the high street. The Task Force provide guidance, tools and skills to help communities, partnerships and local government transform their high streets.

The High Streets Task Force provides support to local leaders in town centres and high streets in England. The website hosts a wide range of training, learning, and data insights, including the COVID-19 Recovery Framework to help places identify what they need to do now, as well as how to plan and build capacity for recovery.

The Task Force has also developed a Routemap to Transformation. As town centres reopen, it is clear that COVID-19 has accelerated change in the high street. Multiple retailers will no longer be the dominant attraction in most town centres and so we have to redefine the high street. The Routemap identifies the steps that have to be taken to make transformation happen. A series of webinars introduces the concept, provides cutting-edge insight from those with experience, and demonstrates what success looks like. These are supported with learning materials and access to resources to enable action.

A list of further guidance document can be found at the end of this report.

Funding sources

Funding can be achieved through a variety of different sources, some available more permanently and others that will run temporarily. Most funds follow societal trends and challenges and have themes attached to them, which stipulate broadly what the money should be used for. It is therefore important to understand a proposed scheme or idea before applying for funding, as this may influence the type of funding you are able to apply for. It is also worth remembering that in most places large parts of town centres will be privately owned and that finding solutions will involve working with the private sector and encouraging investment.

Below is a list of funding sources that are permanent, long-term or currently active. Some funds are new at the time of this publication and it is possible that new funds will emerge. Captured here are funds currently in circulation, although this is not a limited list and there may be other sources.

Active funds (at time of publication)

2019 – various deadlines for each grant, beginning with October 2020 through to September 2021.

This programme supports projects that will contribute to the transformation of high streets and town centres in England helping them become thriving places, strengthening local communities and encouraging local economies to prosper. The fund is for individual heritage buildings in, or transferring to, community ownership. They will support charities and social enterprises to develop projects with the potential to bring new life to high streets by creating alternative uses for redundant or underused historic buildings in town centres.

Running during the financial year 2020 – 2021.

The Government will, in line with the eligibility criteria set out in guidance documents, reimburse councils that pay grants to eligible businesses. These grants are for any small businesses struggling in the context of COVID-19, and are more a preventative measure to stop vacancy occurring.

The Government has set out plans to further the levelling up agenda by launching a new £4 billion Levelling Up Fund that will invest in local infrastructure that has a visible impact on people and their communities and will support economic recovery. The announcement was made on the 25 November 2020 as part of the Spending Review. The Ministry of Housing, Communities and Local Government (MHCLG) is receiving nearly £10 billion of funding in the next financial year and will manage its distribution.

The National Lottery Community Fund

The fund consists of various types of grant, either under or over £10,000, for projects that are responding to the immediate COVID-19 crisis, supporting recovery activity or helping the community to become more resilient in order to respond to new and future challenges. All application deadlines are listed as ‘ongoing’.

Long-term opportunities

Long-term and permanent funding sources are listed below. It should be noted that there may be localised funds available within the local area that are not UK wide, and it would be beneficial to research local opportunities.

As some of the case studies in the framework below highlight, it is possible for the council to directly invest in the scheme with allocated funds (see Telford & Wrekin, see Bath & North East Somerset).

S106 & Community Infrastructure Levy - S106 agreements are private agreements made between councils and developers and can be attached to a planning permission to make acceptable development which would otherwise be unacceptable. These can be in the form of requirements that specified operations or activities to be carried out, requirements that land is used in a specified way, or require a sum or sums to be paid to the authority. A Community Infrastructure Levy is a charge which can be levied by councils on new development in their area. It is an important tool for councils to use to help them deliver the infrastructure needed to support development in their area. Both can be used to fund projects to tackle vacancy in high streets and town centres.

Business improvement districts - A business improvement district (BID) is a geographical area in which the local businesses have voted to invest together to improve their environment. BIDs provide additional or improved services, identified by the local businesses. This could include extra safety, cleaning or environmental measures. BIDs are funded by a mandatory levy on all eligible businesses after a successful ballot. This money is then ring-fenced for use only in the BID area but can be used for regeneration and to increase footfall, which tackling the challenge of vacancy can contribute to.

Community ward funding - Ward budgets are a dedicated and flexible resource within council budgets that councillors can use to support specific local issues and priorities financially. Allocation and use of the funds vary between wards and local priorities. Broadly, councillors can spend this budget flexibly as long as it benefits residents and is supportive of council policy.

Local enterprise partnerships - The LEPs have accountability boards which approve all major funding decisions and monitor and manage the LEPs capital programme for greatest impact, informed by local area management information. LEPs are able to bid for funding from the central government, which can then be awarded to councils through the LEP funding system. Recent examples of a past fund are the local and regional growth deals and Local Growth Fund which was awarded to LEPs and then distributed to projects that benefitted the local area and economy.

Co-op Local Community Fund - The Cooperative choose new causes for communities every 12 months. Applications will open again in Spring 2021.To be accepted the applicant must have a project in mind that will benefit the local community by bringing people together, supporting health and wellbeing or support people to develop skills and build resilient communities.

The National Lottery Heritage Fund - The National Lottery Heritage Fund is the largest dedicated funder of heritage in the UK. Grants from £3,000 to £5million and over are distributed to projects that sustain and transform the UK's heritage. The Fund also provides leadership and support across the heritage sector, and advocates for the value of heritage. The strategic funding framework covers a five year period from 2019 – 2024. This is a rolling programme so there are no deadlines. Applicants can apply when ready, and assessments will be made within eight weeks.

Past funds

In order to properly highlight different types of temporary funding sources, past notable funding sources, that are now closed to new applicants, are listed below. It is worth checking the web pages of the organisations offering the funds, in case new funds are offered:

Future High Streets Fund - This fund was an £830 million package launched in December 2018, with recipients announced on the 26th December 2020. Funding from the Future High Streets Fund will help 72 areas in England to recover from the pandemic and deliver ambitious regeneration plans. The funding will help these areas transform their high streets into vibrant hubs for future generations and to protect and create thousands of jobs.

Stronger Towns Fund - On 6 September 2019 the Government invited 100 places to develop proposals for a town deal, as part of the £3.6 billion Towns Fund. The places were chosen based on a number of factors including declining population often found in residential towns.

Cultural Development Fund - This fund aimed to allow cities and towns to invest in creative, cultural and heritage initiatives that led to culture-led economic growth and productivity. This fund was from the Department for Digital, Culture, Media and Sport (DCMS) that had a budget of £20 million.

High Streets Heritage Action Zone – Sixty eight high streets have been offered funding to give them a new lease of life. The lead partners in each place (mostly councils) are working with Historic England to develop and deliver schemes that will transform and restore disused and dilapidated buildings into new homes, shops, work places and community spaces, restoring local historic character and improving public realm. The High Streets Heritage Action Zone initiative is funded with £40 million from the Department for Digital, Culture Media and Sport (DCMS)’s Heritage High Street Fund and £52 million from the Ministry of Housing, Communities and Local Government (MHCLG)’s Future High Street Fund. A further £3 million has been provided by the National Lottery Heritage Fund to support a cultural programme.

Arts Council England - Arts Council England awards funds from the National lottery, such as the Thriving Communities Fund, which closed on 8 January 2021. This fund was made possible by National Academy for Social Prescribing (providing £1.15 million) and the Arts Council (providing £250,000), the initiative also includes NHS England, Sport England, Natural England, the Office for Civil Society, the Money & Pensions Service and NHS Charities Together as strategic partners. The fund was for activity that enhances collaboration and networking between local organisations, strengthens the range of social prescribing activities offered locally and enables social prescribing link workers to connect people to more creative community activities and services.

Action Framework

High streets and town centres are complex and dynamic mixed-use urban corridors and ensure easy pedestrian access to everyday goods and services, places of work and leisure. They are typically characterised by a variety of premises that accommodate non-residential uses to support the wider neighbourhood. High streets and town centres are linked, and are often synonymous, but high streets can stretch far beyond the town centre boundary and sit outside of designated town centre locations. High streets play an important role in civic and community life and are vital for economic success. Retail is but one part of this.

Vacancy is often a symptom of a wider set of issues that merit sophisticated and sustained consideration and solutions which create new understanding of interrelated issues and promote cooperation between different sectors and partners. Councils and their leaders are in a position to take a broad perspective and bring different interests together in a way that those championing single issues cannot. Further guidance on developing strategies for high streets and town centres can be found at the end of this document in ‘Further guidance’.

Whilst each of the case studies below are varied in their methodologies and intended outcomes, it is important to note that all methods are within the context of the wider place-making role. The good practice examples below are a result of contextual thinking, and as well as tackling vacancy there are wider strategies at play, which in some cases might mean quite a radical transformation of town centres and high streets. It is important to know the wider local needs and opportunities in order to align any strategy that tackles vacancy with the wider priorities of the council.

Case studies

Business/grant funding

Given the typically high levels of private ownership and numerous business stakeholders on high streets and in town centres, grant and loan funding activities to address vacancy is a method that many Local Authorities deploy in order to bring vacant property back into use. In this way, the impact of any individual scheme can be maximised by reaching across multiple sites and ownerships. The funds may come directly from council budgets, or from awarded funding that the council has received externally. Funding may be used to support, for example, external building works, internal fit-out costs or general operational costs (particularly for start-up businesses). Grants or loans can include conditions which allow greater local authority control over outcomes, for example requiring participants to commit to Living Wage employment or achieve a certain Food Hygiene level.

Direct council delivery

Delivery of interventions directly by councils can be targeted at council-owned assets, or may involve privately-owned properties. Clear project management and delivery experience are required in either case, and works may involve commissioning external expertise on, for example, design, architecture or business support. Direct delivery can be an asset in cases where landlords and businesses are reluctant to comply or lack capacity to deliver or support proposals. In some cases, it may be necessary for an authority to gain control of particularly high-profile properties, either through acquisition or securing a lease prior to undertaking activities to address vacancy.

Restoration

In some instances, the factor contributing to long-term vacancy of a property may be its poor physical condition or dilapidation. In this case restoration may be appropriate, particularly so for heritage assets such as Listed buildings. By commissioning the restoration of vacant properties, or working with partners to do so, they can be returned to a lettable condition, either on regular market terms or more favourable ones dependent upon other activities, as covered below.

Meanwhile use/pop-up

Meanwhile and pop-up uses can temporarily fill vacant property until it is permanently brought back into commercial use. Such activities can be relevant to a diverse range of uses and sites, and have potential to provide space for occupiers who may have been squeezed out of high-value areas. This method to fill otherwise vacant property is highly impactful in creating diversity, fostering an environment for testing ideas and ensuring high streets don’t decline in interim periods of development or changing tenancies. Such uses can also be used to test out longer-term aspirations, so whilst they are necessarily short-term in themselves, they can be important components of long-term strategies.

Business support

Small businesses contribute to local economies by bringing growth and innovation to the community. Local Authorities can take an important and influential role in supporting and nurturing this process. Providing business support as a means of tackling vacancy through the provision of free-of charge or affordable space and expert advice allows enterprises to test or establish the feasibility of a business idea or nurture growing businesses. Successful businesses can move on to trade independently from their own premises on the high street, which can contribute to the wider health and sustainability of the town centre.

Policy intervention

In some places, the historic provision of retail floorspace outweighs demand from the local market. Such places are likely to experience long-term vacancy as a consequence of this mis-match in supply and demand. In this case, a clear evidence base in the form of a Retail Needs Assessment (or similar) will provide support for an overall reduction in the amount of town centre floorspace. Such a rationalisation should be clearly controlled by policy, likely at a Local Plan or SPD level to guard against uncontrolled loss of town centre uses. Residential uses are likely to be an appropriate ‘ingredient’ in replacement developments, though the potential for inactive frontages and lack of future flexibility for other uses should be considered in making such plans.

Change of use

The documented decline in retail demand, combined with increasing numbers of empty shops tell us that new uses can and should be introduced into our high streets and town centres. The case studies in this guidance explore a variety of uses such as healthcare and workspace, though other possibilities include education, civic uses, cultural and social infrastructure and residential uses. Empty shops brought back into use for alternative activities can benefit the community and local economy by providing space for community events or workspace for local businesses.

Redevelopment

Multiple ownerships and the complex spatial nature of most high streets makes them quite resilient to blanket redevelopment, but this method to tackle vacancy can be applied where comprehensive ownership can be secured or may be relevant to single units, typically large anchor premises such as former department stores. Such proposals often involve working with a developer or as part of a joint venture, though may – of course – be delivered directly by a council . In these circumstances authorities may be in a development management role to ensure development is compliant with relevant policies, or may be part of the client team to deliver new proposals that rationalise or consolidate retail floorspace and introduce new uses to a site.

Conclusions

Place your strategy within the wider strategic context

Action to target vacancy should not be isolated from wider issues faced by town centres – it is unlikely to be a ‘single issue problem’. Tackling vacancy should sit within wider council priorities and strategies for a high street or town centre. Alignment with council priorities and supportive policies means the scheme will have buy-in from council departments, which is crucial, for example, if the scheme requires planning permission for a change of use.

It is also important to consider the wider ecosystem or context of the area, particularly when the scheme involves regeneration or redevelopment of larger vacant anchor buildings. Having an existing demand driver (a physical hotspot such as existing offices or food outlets) will create a buzz that will attract critical mass and ensure the building acquires a suitable tenant.

Know and be guided by your evidence

Before embarking on a scheme to tackle vacancy, it is important to establish an evidence base that will support the scheme, outline why it is needed, and give a basis from which to monitor impact. Use a Vacant Possession Tracker, record ownership through the Land Registry, record leases, local authority influence and which businesses and facilities are providing community value to better inform action.

Following this, regularly updated research to drive the project forward is key. Not only does it provide supporting data for potential continuation of the scheme, but it also informs the council about which direction the scheme should be taking. This could include an ongoing audit of vacancy levels, the social and economic challenges associated with vacancy, and local perceptions of the town centre. Ideally, schemes should evolve based on this evidence.

Plan for wider impact, not just filling a vacant shop

It is beneficial to have strategies that have a wider social impact beyond addressing vacancy, such as youth engagement and skills training or business support. Proven challenges in securing commercial tenants for properties can lead landlords or local authority asset managers to be more flexible in their approach to rent level and lease terms, e.g. offering social value leases.

Many strategies are a combined response to multiple challenges, for example Warrington Council saw a growing number of vacant properties on the high street but also realised that the local hospital was not equipped to service the local residents. In this scenario, a Health & Wellbeing Hub was set up in a vacant high street property, a single scheme which helped solve both challenges.

Be tactical with marketing and engagement

Consider marketing strategies in two ways; based on and through local engagement and networks and using low cost alternatives such as social media and advertising through partner channels.

Strategies that make use of social media and other low cost marketing techniques should be based on local engagement. For example, using Twitter or Instagram to promote a scheme should be supported by more engagement tactics such as setting up a virtual high street, or running competitions. The marketing strategy should build a buzz as well as identity, capacity and trust with the local community.

Additionally, existing relationships with local organisations should be used to help promote the scheme. If good relationships exist, this will usually mean the council could promote the scheme through these partners social media channels, on the partner website, or physically through banners and posters on partner sites.

Consider your timescales

The case studies above range from fast and responsive actions, such as in Bath and North East Somerset with the introduction of local art commissions into the windows of vacant units, to long-term substantial investments in adaptive re-use of strategic anchor buildings such as the former department store in Sheffield now used as a tech hub. Timescales of the project should be considered; is the local area in need of a quick fix or a long-term solution?

In the long term many councils are considering consolidation of retail space in high streets and town centres by introducing other uses. Consolidating the retail offer can create a more manageable and focused centre, and therefore reduce the risk of empty property. Whilst residential could be one alternative use for the properties outside of the consolidated area, there are also key risks and challenges that come with this, such as inactive frontages and lack of flexibility for future use. Alternative uses for town centre property outside could be cultural hubs, shared workspace or other uses that promote social value.

Engage absent landlords

Ownership of land is searchable through the Land Registry, and the owner of vacant property - if they don’t come forward or are not known by the council - can be found in this database. Engaging absent landlords is a key challenge, but they can be engaged and brought onto a scheme with a number of tactics outlined in the case studies above, such as offering to update the facade of the unit in return for its use, or by reaching out through a council project with alternative branding in the event the landlord is unwilling to engage with the council directly.

Be tactical in which powers your using

These examples have shown the key role that councils can play in bringing together diverse high street stakeholders to tackle the issue of vacancy. Strategic policy setting and decision-making are highly influential, particularly with regard to long-term change. However, softer powers such as building partnerships or delivering temporary uses can also be essential as more agile responses to a rapidly changing retail context. In particular, the ability to secure and distribute funds often underpins successful strategic action that may be felt across multiple property ownerships or areas. Many of our case study examples adeptly combine hard and soft powers available to authorities to bring about meaningful strategic change.

Understand your council’s skill set

Many of the case studies above highlight the need for particular in-house skills that are necessary to carry out the programme or scheme. For example, internal marketing and communications teams, technical skills in building a virtual high street, workspace managerial experience or skills and knowledge in putting together funding applications are all ‘in-house’ skills represented in the case studies above. Consider which skills are available and what the strengths and weaknesses are of the internal teams, as well as which people with particular skills will be available to work on the project. Understanding available skills and applying them to the proposed project will have a positive impact on its success.

In the case of Tyne and Wear council , an external team was brought in to manage and carry out restoration work as well as engaging the local community and securing tenants once the restoration work was complete. A tactical approach to tackling vacancy therefore would be to partner with a special agent, to either tackle local authority capacity issues or fill council skills gaps. This could be from employing a specialist company to carry out marketing and engagement, to working with a tech firm for digital skills, to partnering with a developer to carry out redevelopment.

Further guidance

‘Building on Strong Foundations: A Framework for Local Authority Asset Management’, Department for Communities and Local Government, 2008

‘Empowering Communities: Making the Most of Local Assets’, Local Government Association, 2012

‘Open for Business: Empty Shops on London’s High Streets’, London Assembly, 2013

‘People, Culture, Place - The Role of Culture in Placemaking’, Local Government Association, 2017

‘High Streets for All’, Greater London Authority, 2017

‘Revitalising Town Centres, a Handbook for Council Leadership’, Local Government Association, 2018

‘Revitalising Town Centres, a Toolkit for Councils’, Local Government Association, 2018

‘Culture-Led Regeneration: Achieving Inclusive and Sustainable Growth’, Local Government Association, 2019

Meanwhile Use London, Greater London Authority, 2020

‘Town Centre Checklist: A Self-Assessment Tool’, Local Government Association, 2020

‘Creative Places - Supporting Your Local Creative Economy’, Local Government Association, 2020

‘High Streets & Town Centres, Adaptive Strategies’, Greater London Authority, 2020