Introduction

Councils are responsible for their own performance and improvement. This is recognised in the ‘sector-led improvement’ approach which is underpinned by the key principles that councils:

- are primarily accountable locally, not nationally

- have a sense of collective responsibility for the performance of the local government sector.

The LGA’s role is to provide tools and support councils and also to maintain an overview of the performance of the sector.

To comply with the Best Value Duty to secure continuous improvement in the way the authority’s functions are exercised, each council must take appropriate measures to gain assurance both of the performance of its services and of its corporate governance.

Through a focus on effective assurance, councils can mitigate the risks and costs of failure and their impacts on local residents and businesses.

This framework aims to:

- support councils to understand how to use the components within the framework and how they fit together

- increase the effectiveness of assurance in the sector. While it cannot itself prevent failures, its use may reduce the risk – and costs - of statutory or non-statutory intervention, whether by central government or other regulators;

- make it easier for local residents and businesses to understand how to hold their local authority to account.

Assurance may sometimes be seen as a dry topic, and accountability may, wrongly, be feared. However, the management and routine operation of internal controls and risk management support councils to manage the future constructively and safely. As one council leader said, ‘it’s what helps me to sleep at night’.

All members have a responsibility to oversee effective governance, and all officers have a duty to comply with good governance and provide information to demonstrate that compliance.

Not all of the components of the system are currently working as well as they should. In the context of the continuing crisis in local audit, it is more important than ever that councils should undertake their own assurance activities effectively. The LGA will continue to work with its partners to seek to ensure continuous improvement of the system and all of its components.

Elected members play a crucial and continuous role in seeking assurance of the council’s activities and governance. This includes assurance of each council’s own local objectives, for which they are accountable to their local electorate.

Councils will rightly make political choices in response to local circumstances: successful authorities make these choices within the context of good management practice, consideration of cost-effectiveness and value for money, robust controls and risk management.

Councils exist to improve the quality of life of, and the quality of places for, the communities they serve. Therefore, the focus of councils’ assurance work is on the assurance they provide to local communities.

This framework includes the key components of local authority assurance. Many of these are processes and structures. The framework also includes organisational culture, behaviours and ways of working.

There is a crucial role for political and managerial leaders in challenging poor behaviour (in both formal and informal settings) and non-compliance.

What is the scope and status of this framework?

The framework is applicable to unitary, county, district and borough councils in England, and to English authorities with all types of governance system.

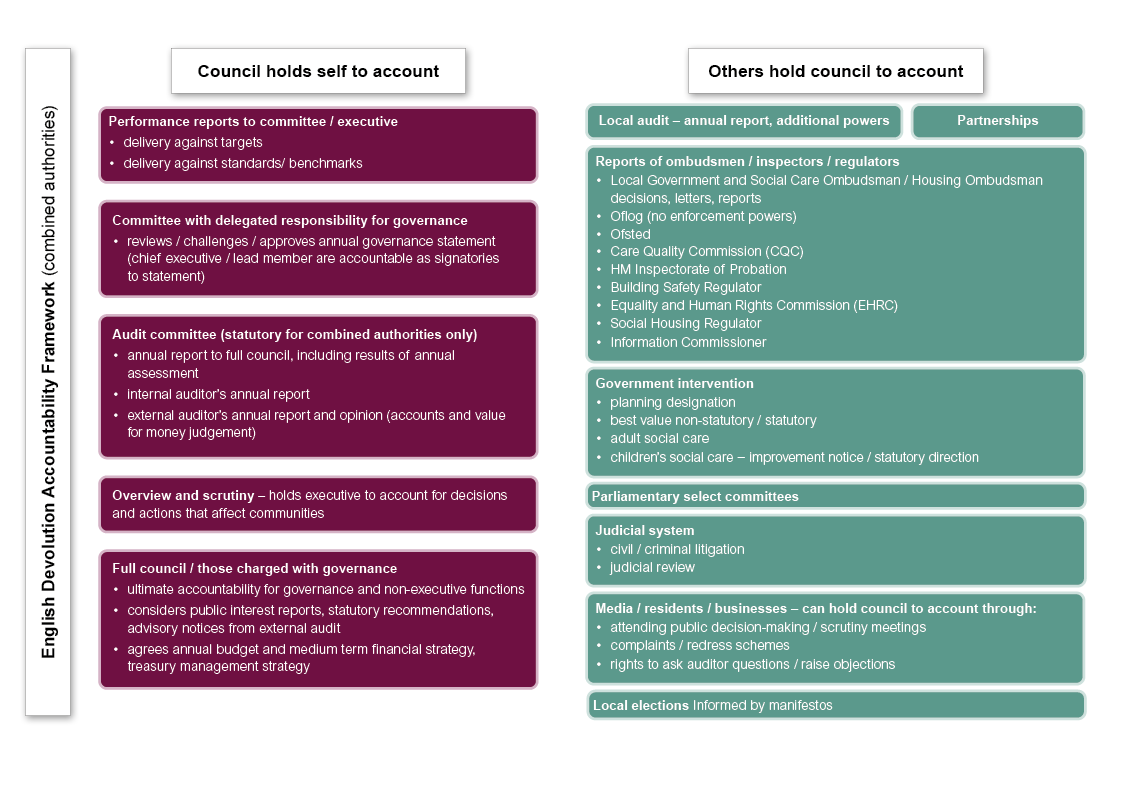

The specific assurance requirements for combined authorities are set out in the English Devolution Assurance Framework but the principles in this framework will apply to combined authorities too.

The framework is part of a suite of guidance, tools and resources for the sector produced by the LGA and other bodies. Effective assurance is achieved mainly through the application of best practice rather than statutory activity, although the framework points to statutory provisions where relevant.

Failure in one service area may impact significantly on the whole organisation. This framework focuses on corporate areas and overarching governance, rather than including every service-specific source of assurance. Each service area will have its own mechanisms for assurance and accountability and councils will need to assure themselves of compliance with statutory duties in each case. Effective corporate assurance will support assurance of individual services and the principles and good practice identified in this framework will apply to all services as well as corporate activities.

What is the relationship between this framework, corporate peer challenge, best value standards and statutory interventions?

At any one time, each local authority will be at a point on a continuum. At one end are authorities which have a strong awareness of their strengths and areas for development, are proactive in seeking opportunities for improvement and delivering best value (even where performance is strong) and elected members and officers take appropriate actions to assure themselves in relation to their performance and governance.

The characteristics of a well-functioning authority set out in the best value standards include effective use of many of the framework’s components: equally, the standards’ indicators of potential failure may arise where assurance activity is not effective. A failure to deliver best value is, essentially, a failure of governance.

At the other end, a small minority of authorities are not sufficiently self-aware, do not take effective action to achieve continuous improvement, do not have effective assurance arrangements and consequently have entered statutory intervention. Local authorities can and do move between points on this continuum over time.

The LGA works with regional groupings of councils, professional bodies and others to support as many local authorities as possible to stay at the positive end of the continuum, aiming to prevent authorities from moving towards the ‘intervention’ end, so that they continue their improvement journey even further.

The LGA’s corporate peer challenge is one of the improvement tools that councils can use as part of their assurance of their own performance and governance, so that they can address their own challenges where possible without central government or regulators needing to become involved.

What do we mean by assurance?

We have developed the following definition through consultation with the sector:

Timely and accurate information, evidence and evaluation of how local authorities are delivering their duties, functions and outcomes, which can be used to hold them to account and may give confidence.

There should be no assumption that assurance will always be gained, particularly as the scale of challenges facing local government increases.

A ‘not assured’ outcome, as long as it is acted upon, may be as valuable to an authority as ‘assured’. Where positive assurance is not possible there is support available, from the LGA and from others in the sector, to help the council put things right.

By using the assurance system and its components effectively, councils can increase their chances of identifying issues and addressing them before they get more difficult – and costly – to fix. The cost of statutory intervention can be far greater than the cost of sector support.

Assurance cannot be gained ‘by numbers’ or a one-off event: there is no simple list of yes/no indicators which will help a council decide whether or not it can be assured of its performance or governance.

It is achieved through a series of nuanced, qualitative and triangulated judgements, to gain a view of the council in the round.

What do we mean by accountability?

The Review of Audit and Accountability defined accountability as:

…the requirement to provide explanations about the stewardship of public money and how this money has been used.

There are multiple elements of accountability in local government, for example:

- councillors to their constituents

- the executive (cabinet), where relevant, to the overview and scrutiny function

- the executive, where relevant, and the organisation to the audit committee

- officers to the council (through line management)

- specific statutory officers to the full council (through reporting responsibilities)

- officers to their professional bodies in relation to professional standards and conduct (where applicable)

- the council for its stewardship of public resources (through external audit)

- the council to ombudsmen / inspectors / regulators

- the council to the courts/ redress schemes

- the council to wider partnerships, bodies and authorities.

Components of the framework

The key components of the improvement and assurance framework for local government are set out in the following categories, shown diagrammatically through the links below:

- Actions to contribute to assurance of local authorities, by:

- officers, not usually in public

- members and officers, sometimes but not always in public

- members and officers, in public

- other bodies, not usually in public

- Local authorities’ public accountability:

- the authority holding itself to account

- others holding the authority to account.

Some of these components:

- are required by legislation;

- include a mixture of legislative requirements and best practice;

- reflect practice which is not set down in statute but is necessary in a well-run authority;

- reflect content from the best value standards and/or reports relating to ‘failed’ councils which identify where key activities were absent or poorly performed.

More information about each component, with links to relevant guidance and improvement support, appears below.

Engagement with sector support is itself a key component of the framework, whether from other authorities, regional, national and/or professional bodies. The LGA’s regional teams include member peers who can advise on a range of support for local authorities which will help understanding and implementation of the assurance activities shown below. This includes bespoke support and mentoring in addition to:

- councillor and officer development

- top team development

- corporate, finance and governance peer challenges

- transformation tools and support

In addition to considering what the key components are, read on to consider how they are implemented, with information about key principles and what good looks like.

The ‘three lines’ model

The ‘three lines model’ outlines the different contributions that different sources of assurance can provide:

| First line |

Actions by managers and staff who are responsible for identifying and managing risk as part of their day-to-day management and delivery of services. This includes:

|

|---|---|

| Second line |

The way the authority oversees the effectiveness of its controls so that it operates effectively, for example, the responsibilities of:

|

| Third line | Independent assurance, such as internal audit. Accountable to Full Council. |

| Governing body | Full Council |

| External assurance providers |

For example:

|

There should be regular dialogue and coordination between the different ‘lines’ and escalation where appropriate.

What actions contribute to assurance of local authorities by officers (not normally in public)?

Open a larger version of this diagram

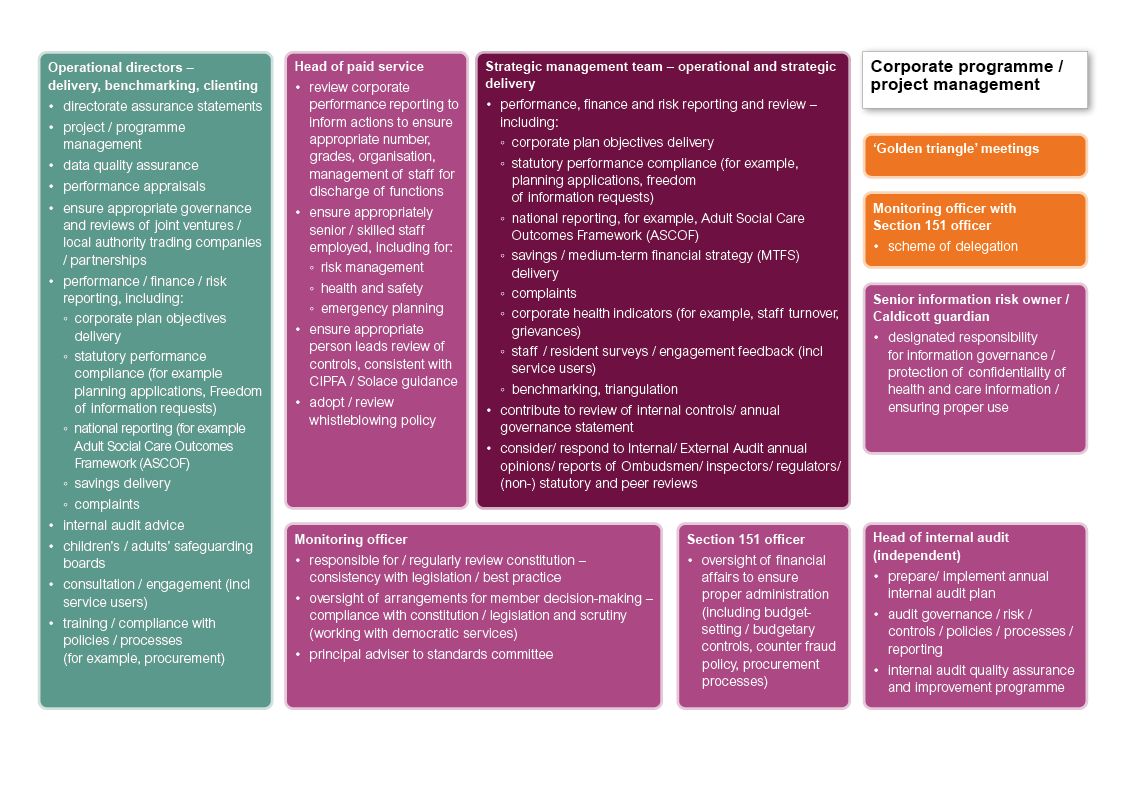

What should you expect of key officers?

- The chief executive (head of paid service):

- is responsible for ensuring the appropriate number, grades, organisation and management of staff for the discharge of the authority’s functions

- ensures appropriately senior and skilled staff are employed, including for:

- risk management

- health and safety

- emergency planning and business continuity

- and that these arrangements are appropriately managed and coordinated:

- ensures that an appropriate person leads the review of the effectiveness of the authority’s governance arrangements to inform the annual governance statement

- ensures the adoption, effectiveness and regular review of the authority’s whistleblowing policy.

- The monitoring officer:

- regularly reviews the constitution to ensure that it reflects both legislation and good practice (working with Democratic Services)

- oversees arrangements for member decision-making, ensuring their compliance with the constitution and legislation

- acts as principal adviser to the Standards Committee.

- The chief finance officer is responsible for ensuring proper administration of the authority’s financial affairs (including budget-setting, budgetary controls, procurement practices and the authority’s counter-fraud policy).

- The head of paid service, monitoring officer and chief finance officer act together as the ‘Golden Triangle’ to ensure and support good governance in the authority.

- The strategic management team effectively oversees operational and strategic delivery, including:

- reporting and review of performance, finance and risk, including:

- delivery of corporate plan objectives

- compliance with statutory requirements and national outcomes frameworks

- delivery of budget savings and medium term financial strategy

- responses to and learning from complaints

- corporate health indicators (for example, staff turnover, grievances)

- staff and resident surveys and feedback from service user and community engagement

- benchmarking with relevant organisations

- considering and responding to annual reports by internal and external audit, ombudsmen, inspectors, regulators and peer reviews, and statutory/ non-statutory reviews.

- reporting and review of performance, finance and risk, including:

In addition to considering all of the above individually, it is essential that the strategic management team consider the cumulative impact where limited or no assurance is possible in relation to more than one issue or service.

- The head of internal audit provides independent assurance by:

- preparing the annual internal audit plan, informed by risk in the authority, and implementing that plan;

- auditing the authority’s governance, risk management, controls, policies, procedures and reporting;

- developing and implementing the internal audit quality assurance and improvement programme, including external assessment against the Public Sector Internal Audit Standards.

Open a larger version of this diagram

What is members' role?

All members have a responsibility to oversee and assure effective governance and accountability.

- The Executive (Cabinet) / Policy and Resources Committee reviews performance, finance and risk reporting at a strategic level, including:

- delivery of corporate plan objectives

- compliance with statutory requirements and national outcomes frameworks

- delivery of the medium term financial strategy

- corporate health indicators (for example, staff turnover, grievances).

Reporting should be regular: good practice would be at least quarterly.

- The Executive (Cabinet) / Policy and Resources Committee holds itself to account for delivery against performance targets, standards and benchmarks.

- In authorities with the executive governance model and those with the committee system which choose to appoint them, overview and scrutiny committee(s):

- review performance/ finance/ risk reporting

- undertake pre-decision and/or budget scrutiny

- call-in executive decisions

- undertake scrutiny reviews in order to support policy development or consider and review strategic options.

- Overview and scrutiny committees hold the Executive (Cabinet) to account for the decisions and actions that affect local communities.

- The work of scrutiny is supported by the statutory scrutiny officer.

- When reviewing finance and risk issues, scrutiny will need to have regard both to the work of the audit committee but also to the executive’s own role in oversight and assurance.

- There is statutory guidance which sets out how effective overview and scrutiny should be conducted, and support and further guidance is available from the Centre for Governance and Scrutiny. For devolved areas, a scrutiny protocol provides further detail.

- The Appointments Committee recommends to full council the appointment of appropriately qualified statutory officers.

- The Audit Committee:

- monitors and reviews the effectiveness of the authority’s internal controls, risk management and financial reporting holds internal and external audit to account

- approves the internal audit plan, ensuring that it is informed by the strategic risks facing the authority. It oversees the plan’s implementation and ensures compliance with the Public Sector Internal Audit Standards

- reviews internal and external audit reports and opinions and oversees management responses

- assesses its own practice (an annual external review is recommended)

- may include lay members to provide additional expertise

- holds management to account in relation to the opinions of internal and external audit and for the implementation of their recommendations

- is held to account by Full Council through an annual report, which should include reference to a self-assessment of its own performance.

CIPFA provides more detailed guidance, including terms of reference for Audit Committees.

The LGA provides a range of support for audit committees:

- Ten questions for audit committees to ask.

- Audit Committees: Leadership Essentials.

- Regional audit forums for audit committee chairs provide an opportunity to access training, share good practice and discuss common issues. Email for more information.

The Centre for Governance and Scrutiny has produced guidance on the respective roles of audit and scrutiny committees.

- The committee with delegated responsibility for governance:

- reviews the draft annual governance statement

- holds management (via the chief executive and lead member as signatories) to account for implementation of improvement actions identified in the annual governance statement

- oversees regular reviews of the constitution.

- Standards Committee:

- reviews the member code of conduct and arrangements for investigating complaints into member conduct to ensure compliance with the Nolan Principles

- reviews the monitoring officer’s annual report

- seeks the perspective of the committee’s Independent Person(s).

In many authorities the committee is also responsible for overseeing the development and implementation of programmes of member training, ensuring their appropriateness and take-up by members. If this is not within the remit of Standards Committee, the authority will need to ensure that another member-level body has that remit.

The role of Standards Committee as part of the governance framework is distinct and should be separate from that of the Audit Committee which oversees the effectiveness of that framework.

- Full Council is the body charged with the governance of the council and while it may delegate some responsibilities it remains accountable and therefore should seek assurance. It does this by:

- considering the s.25 statement of the chief finance officer of the robustness of estimates and adequacy of reserves before approving the budget

- reviewing (at least) an annual report from each of the chairs of the Overview and Scrutiny Committee (where relevant), Audit and Standards Committees and holding them to account

- appointing appropriately qualified statutory officers

- consideration of the external auditor’s annual report also represents good practice and ensuring appropriate responses to public interest reports, statutory recommendations and advisory notices from external audit.

- Corporate statutory officers have a range of individual statutory duties to report to Full Council. These include, but are not limited to, the chief finance officer reporting actual or potential unlawful expenditure or an unbalanced budget (through a ‘Section 114’ notice), the monitoring officer reporting maladministration and the head of paid service reporting on the arrangements for the discharge of the authority’s functions.

Key principles of good assurance and accountability

- Clarity: understand who is accountable for what. Is it easy to see in your council’s constitution who can take which decisions? Do the people who have key roles relating to assurance in your council have a shared understanding of those roles and have they had appropriate training?

- Proportionality: assurance activity must add value, be cost-effective and be proportionate to the level of risk. As risk changes, so should the council’s assurance activities, both at a strategic level and in relation to specific high-risk activities.

- A whole-council approach: All members have a responsibility to oversee effective governance, and all officers have a duty to comply with good governance and provide information to demonstrate that compliance. Everyone should understand their contribution, and this may include partners and other stakeholders.

- A culture of assurance and accountability, with a low tolerance for poor governance/ performance: ‘The culture of any organisation is shaped by the worst behaviour the leader is willing to tolerate’ (School culture rewired, Gruenert and Whitaker). Councils which entered statutory intervention had many of the right processes in place, but cultures which tolerated non-compliance, including poor behaviours. In some places there was a lack of curiosity and intolerance of internal challenge to norms: while trust is important, so is constructive challenge.

- Monitoring against standards, benchmarks and local targets: some elements of what good performance looks like change over time: understanding how the authority performs in terms of value for money should be a constant endeavour. In addition to local targets, many council service areas will have standards against which they are measured: reporting to elected members should include performance against these. LG Inform is freely available to all and enables any council’s performance to be compared with any other council or group of councils.

- Credible, quality data and information: elected members and the public can only be assured where they are confident in the quality of the information on which assurance judgements are based.

- Transparency, accessibility and intelligibility of information: a commitment to transparency is a fundamental element of good governance. Access to information for elected members.

- Seeking and engaging with external challenge and support: there are multiple opportunities for peer challenge and support at (sub)regional and national levels, for individual services and at a corporate level. The LGA’s peer challenge programme supports continuous improvement by providing insight, guidance and challenge as well as assurance to local leaders and residents.

- Independent assurance: assurance should be proactively sought from a variety of sources. All of the corporate statutory officers, in particular, should be prepared to approach audit (whether internal or external, both are independent) with any concerns and seek their advice, in addition to commissioning audits of specific activities or programmes. Where risks are significant, the council should consider seeking additional external assurance from relevant experts.

What does ‘good’ look like?

Good practice in local government assurance includes:

- Visible, collective ownership and leadership of good governance by both political and managerial leaders. All members and officers should be able to see that the council’s political and managerial leadership prioritise assurance activity and accountability. This includes taking difficult decisions as and when necessary. The Leadership Academy and Leadership Essentials support the development of political leadership skills.

- Being a learning organisation. Continuous improvement requires continual learning and development. Self-awareness is an essential first step, with a recognition of both strengths and areas for development. Organisations which guard against complacency are less likely to be caught by ‘unknown unknowns’. Openness to external challenge and a lack of defensiveness are also prerequisites. Continuing professional development is essential for both the authority’s political leadership and corporate statutory officers.

- Assurance as a constant process, not a one-off event. The external auditor’s annual report mainly looks back at previous activity, and internal audit reports capture practice at a moment in time. Ensuring consistent use of processes and engagement with training, and use of monitoring information can help provide assurance between bigger assurance ‘events’.

- Assurance supports the achievement of priority outcomes. Assurance is not an end in itself. A culture of assurance and accountability is more likely to be embedded where elected members and officers understand that assurance activity keeps the council ‘safe’ and able to deliver for residents.

- Making it easy for the public to hold the council to account. This includes communicating well with the public on the council’s performance and ensuring public understanding of and access to key accountability opportunities and assurance information. Local authorities must also comply with the Transparency Code.

We have collected some case studies which give examples of recent good practice in councils.

How was this framework developed?

The LGA has consulted with local authorities, professional bodies and other key stakeholders to prepare this framework and supporting guidance, which has been informed by draft guidance on best value standards and intervention and learning from recent council failures.

The LGA will continue to develop it over time as new insights and best practice are identified, reviewing the framework at least annually. Tools and training to support its implementation will also be developed by the LGA and partners.

Glossary of terms

Accountability: the requirement to provide explanations about the stewardship of public money and how this money has been used.

Annual Governance Statement: an annual report prepared, approved and published with the financial statements that describes the effectiveness of the council’s overall governance arrangements and an action plan to improve them.

Assurance: timely and accurate information, evidence and evaluation of how local authorities are delivering their duties, functions and outcomes, which can be used to hold them to account and may give confidence.

Assurance statement: a statement providing evidence and confidence that an internal control(s) and/or service is operating in an effective way, in line with any statutory duties and/or best practice.

Best Value: the legal duty introduced in the Local Government Act 1999 that requires local authorities to make arrangements to continuously improve the way in which their functions are exercised and to have regard to a combination of economy, efficiency and effectiveness. Best Value Standards and Intervention: a statutory guide for best value authorities (section 5).

Corporate statutory officers: three corporate statutory officers within all councils, the head of paid service, chief finance officer and monitoring officer, who each have distinct legal roles and responsibilities and work together to ensure the effectiveness of the council’s corporate governance and assurance.

Operational directors: officers with overall responsibility for managing a service. Legislation requires local authorities to have some but not all posts, for example, Directors of Public Health are statutory roles, whilst Directors of Transport are not.

{kind=link}

{kind=link}

{kind=link}

{kind=link}